Ask The Wizard #273

I have some match play chips. Unlike the usual case, the casino in question allows them to be used in any game. What bet would you recommend I use them on?

That is unusual. Said casino probably has no clue what they are doing. For the benefit of other readers, let me review what a match play chip is. These are chips that you match with real money when making a bet. If you win, you are paid on both, and your real money wager is returned. If you lose, you lose both. Nothing happens on a push.

So a match play chip may be used only once on a resolved bet. If the casino allows you to use it on any bet, the proper strategy is to put it on a long-shot bet. This is because the cost of not getting the match play back after a win is a lot less on a long-shot bet than an even-money wager.

The following table shows various bets in three different games and the expected number of units won. For the purposes of the table, it is assumed if the player gets a tie he keeps repeating the same bet until it is resolved. You can see the highest expected value is on a single-number bet in roulette at 87% of face value.

Match Play Expected Value

| Game | Bet | Pays | Probability | Return |

|---|---|---|---|---|

| Baccarat | Banker | 1.9 | 0.506825 | 0.469792 |

| Baccarat | Player | 2 | 0.493175 | 0.479526 |

| Baccarat | Tie | 16 | 0.095156 | 0.617651 |

| Craps | Pass | 2 | 0.492929 | 0.478788 |

| Craps | Don't pass | 2 | 0.492987 | 0.478961 |

| Craps | Easy hop | 30 | 0.055556 | 0.722222 |

| Craps | hard hop | 60 | 0.027778 | 0.694444 |

| Roulette | 18 numbers | 2 | 0.473684 | 0.421053 |

| Roulette | 12 numbers | 4 | 0.315789 | 0.578947 |

| Roulette | Six numbers | 10 | 0.157895 | 0.736842 |

| Roulette | Four numbers | 16 | 0.105263 | 0.789474 |

| Roulette | Two numbers | 34 | 0.052632 | 0.842105 |

| Roulette | Single number | 70 | 0.026316 | 0.868421 |

Please explain what an APR interest rate is.

APR stands for Annual Percentage Rate. The purpose of it is to equate an interest rate with possible points and compounded monthly to an APY (annual percentage yield), which is an interest rate with no points and compounded annually.

For those who don't know, when you take out a mortgage, the bank often charges a finance fee based on the amount of the mortgage. For each point, the borrower must pay 1% of the mortgage amount to the bank as an additional fee. Sometimes this fee is tacked on to the principal amount.

The APR interest rate is hypothetical. If the borrower negotiated with the lender to increase the interest rate, in exchange for no points, and compound interest annually, then the APR interest rate would result in exactly the same payment. Let's look at an example.

Suppose the borrower wants a loan of $250,000. The bank charges 5.625% interest, compounded monthly, with two points, based on a 30-year mortgage. What would be the APR? The finance fee is 2% of $250,000, which equals $5,000. The borrower then asks the bank to add that to the principal, for a loan of $255,000. I won't get into the monthly payment calculation, so take it on faith that it comes to $1,467.92.

Assuming there were no points, an interest were compounded annually, what interest rate would equate to the same monthly payment of $1,467.92 on a loan of $250,000? By trial and error I find an interest rate of 5.9635% and no points and compounded annually results in the same monthly payment of $1,467.92. So, a way to phrase this would be, "A 30-year fixed loan at 5.625% interest with two points has an APR of 5.9635%."

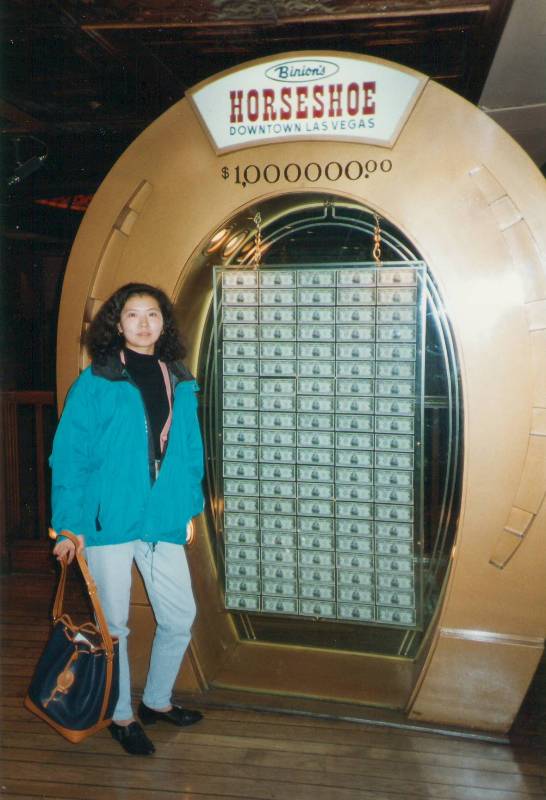

I am suspicious whether the $1,000,000 display at Binion's in Las Vegas really contains one million dollars. If it were all hundred dollars bills, then it should have a lot more. Maybe it is just a hoax and there are all $1 bills in the middle. What do you think is in the middle, sandwiched between the hundreds in the front and back?

I have no reason to doubt there is a million dollars under that case. Their older, and much better, display clearly had one million in the form of 100 $10,000 bills. For those unfamiliar with them, $10,000 bills are extremely rare and sell for about ten times that at auction. Another reason I don't doubt they have a million dollars on the premises is every Nevada casino has to have sufficient cash to do business, and I imagine the Nevada Gaming Control Board lets Binion's count the money in that display, as a last resort. Ironically, not having sufficient cash on hand was the reason Binion's was closed down in 2004 (source).

To get back to your question, it would take 10,000 $100 bills to make a million dollars. Given that a bill is 6" long and 2.625" high, and a 100-bill stack is about 1/2" high, a million dollars would occupy 787.5 cubic inches only. That is just 46% of a cubic foot. You could fit a million dollars in $100 bills in a briefcase easily. So clearly there are some non-$100 bills in that case.

Discussion about this in my forum turned up an article with the specifics, Recurring currency from the Aug. 22, 2008 Las Vegas Review Journal. It says that the display has 42,000 $1 bills, 34,400 $20 bills, and 2,700 $100 bills.

This question was raised and discussed in the forum of my companion site Wizard of Vegas.

The carrier rate of Cystic Fibrosis of those of European descent is 1 in 25 people (source: Wikipedia). Assuming that nobody positive for Cystic Fibrosis will reproduce, and no incest, and a constant period of time between generations, how many generations will it take for this rate to be reduced in half, or to 1 in 50 people?

Before I answer that, let me review recessive disease genetics, which is the case with Cystic Fibrosis (CF). Humans have two copies of each gene, one from the mother and one from the father. When there is a mating, the offspring will randomly inherit one each from the father and mother, resulting in two genes of his/her own.

In the case of CF, it takes two positive genes to be positive. In the case of one positive and one negative gene, the negative one will dominate. In such an event, the person is a carrier, negative for CF, but has a 50% chance of passing on the positive CF gene. Two negative genes will result in being completely clean of CF.

Given that both parents are carriers, here is the probability of each possible outcome for their offspring:

Positive: 0.5×0.5= 0.25

Carrier: 0.5×0.5 + 0.5×0.5 = 0.5

Negative: 0.5×0.5 = 0.25

Given one carrier and one negative parent, here is the probability of each possible outcome for their offspring:

Positive: 0

Carrier: 0.5×1 = 0.5

Negative: 0.5×1 = 0.5

Given two negative parents, the offspring will be negative with 100% chance.

Let's define the probability of the three possible states as:

p = positive

c = carrier

n = negative

Given random parents, let's solve for each after one generation.

p = pr(two carrier parents)×pr(positive given two carrier parents) +

pr(one carrier parent)×pr(positive given one carrier parents) +

pr(zero carrier parents)×pr(positive given two carrier parents) =

c2 × 0.25 + 2×c×(1-c)×0 + (1-c)2×0 = c2/4.

c = pr(two carrier parents)×pr(carrier given two carrier parents) +

pr(one carrier parent)×pr(carrier given one carrier parents) +

pr(zero carrier parents)×pr(carrier given two carrier parents) =

c2 × 0.5 + 2×c×(1-c)×0.5 + (1-c)2×0 = c-c2/2.

n = pr(two carrier parents)×pr(negative given two carrier parents) +

pr(one carrier parent)×pr(negative given one carrier parents) +

pr(zero carrier parents)×pr(negative given two carrier parents) =

c2 × 0.25 + 2×c×(1-c)×0.5 + (1-c)2×1 = c2/4 - c + 1

So the probability of being a carrier, given not positive is:

(c - c2/2)/ (1 - c2/4) =

(4c - 2×c2)/(4 - c2) =

[2c×(2-c)] / [(2-c)×(2+c)] =

2c/(2+c)

We were given that the carrier rate now is 4%, so in one generation it will be 2×0.04/(2+0.04) = 3.92%.

The following table applies this formula for 100 generations.

Cystic FibrosisCarrier Rate

| Generation | Rate |

|---|---|

| 0 | 0.040000 |

| 1 | 0.039216 |

| 2 | 0.038462 |

| 3 | 0.037736 |

| 4 | 0.037037 |

| 5 | 0.036364 |

| 6 | 0.035714 |

| 7 | 0.035088 |

| 8 | 0.034483 |

| 9 | 0.033898 |

| 10 | 0.033333 |

| 11 | 0.032787 |

| 12 | 0.032258 |

| 13 | 0.031746 |

| 14 | 0.031250 |

| 15 | 0.030769 |

| 16 | 0.030303 |

| 17 | 0.029851 |

| 18 | 0.029412 |

| 19 | 0.028986 |

| 20 | 0.028571 |

| 21 | 0.028169 |

| 22 | 0.027778 |

| 23 | 0.027397 |

| 24 | 0.027027 |

| 25 | 0.026667 |

| 26 | 0.026316 |

| 27 | 0.025974 |

| 28 | 0.025641 |

| 29 | 0.025316 |

| 30 | 0.025000 |

| 31 | 0.024691 |

| 32 | 0.024390 |

| 33 | 0.024096 |

| 34 | 0.023810 |

| 35 | 0.023529 |

| 36 | 0.023256 |

| 37 | 0.022989 |

| 38 | 0.022727 |

| 39 | 0.022472 |

| 40 | 0.022222 |

| 41 | 0.021978 |

| 42 | 0.021739 |

| 43 | 0.021505 |

| 44 | 0.021277 |

| 45 | 0.021053 |

| 46 | 0.020833 |

| 47 | 0.020619 |

| 48 | 0.020408 |

| 49 | 0.020202 |

| 50 | 0.020000 |

| 51 | 0.019802 |

| 52 | 0.019608 |

| 53 | 0.019417 |

| 54 | 0.019231 |

| 55 | 0.019048 |

| 56 | 0.018868 |

| 57 | 0.018692 |

| 58 | 0.018519 |

| 59 | 0.018349 |

| 60 | 0.018182 |

| 61 | 0.018018 |

| 62 | 0.017857 |

| 63 | 0.017699 |

| 64 | 0.017544 |

| 65 | 0.017391 |

| 66 | 0.017241 |

| 67 | 0.017094 |

| 68 | 0.016949 |

| 69 | 0.016807 |

| 70 | 0.016667 |

| 71 | 0.016529 |

| 72 | 0.016393 |

| 73 | 0.016260 |

| 74 | 0.016129 |

| 75 | 0.016000 |

| 76 | 0.015873 |

| 77 | 0.015748 |

| 78 | 0.015625 |

| 79 | 0.015504 |

| 80 | 0.015385 |

| 81 | 0.015267 |

| 82 | 0.015152 |

| 83 | 0.015038 |

| 84 | 0.014925 |

| 85 | 0.014815 |

| 86 | 0.014706 |

| 87 | 0.014599 |

| 88 | 0.014493 |

| 89 | 0.014388 |

| 90 | 0.014286 |

| 91 | 0.014184 |

| 92 | 0.014085 |

| 93 | 0.013986 |

| 94 | 0.013889 |

| 95 | 0.013793 |

| 96 | 0.013699 |

| 97 | 0.013605 |

| 98 | 0.013514 |

| 99 | 0.013423 |

| 100 | 0.013333 |

Half the current 4% rate is 2%. You can see from the table that that will be achieved in 50 generations. Assuming 30 years per generation, that will take 1,500 years.